/grid-img-thumb-3-(12).png)

Precision in Patent Distributions:

SMU’s and Inventor’s Shares

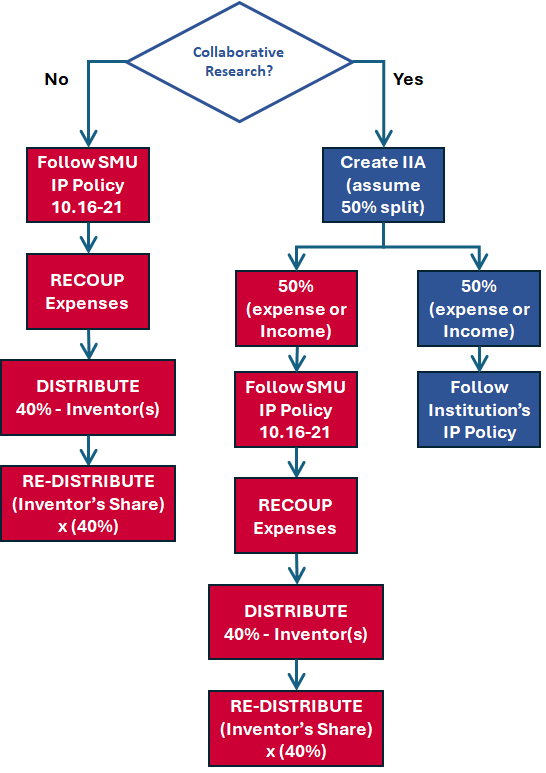

How prosecution expenses and any net benefits (income) are to be divided must be defined before expenses or income are generated. First consideration is the division between SMU and another University (or other Universities). The division between SMU and its faculty inventors is set by SMU IP Policy.

The Inter-Institutional Agreement (IIA) defines the split between SMU and another institution. Although the percentages and responsibilities associated are negotiated with the other institution independently for each IIA, the common topics are the division of expenses and royalty income from licensing the invention.

If the research is Collaborative, it is very important to establish the distribution and responsibilities first through the IIA.

If there is no collaborating institution, the expense reimbursements and royalties are distributed according to SMU’s IP Policy found in Section 10.16-21.

The portion of a royalty payment shared with the inventor(s) is distributed according to the Distribution Percentages as found in the percentage distribution for each patent in Sophia.

SMU’s INVENTOR DISTRIBUTION

The SMU IP Policy, Section 10.16-21, has the following Inventor Distribution matrix.

| $0-100K | $100-500K | Above $500K | |

| Inventor(s) as personal property | 40% | 35% | 30% |

| University: | 60% | 65% | 70% |

| Recovery of Overhead | 10% | 10% | 10% |

| Office of the Dean of Research | 20% | 25% | 30% |

| Office of the Dean of the College or School originating the Patent | 20% | 20% | 20% |

| Inventor(s) responsible for Patent (for Lab) | 10% | 10% | 10% |

The Inventor(s) as Personal Property means the percentage of the royalty directly paid the inventor(s). This percentage changes depending on the amount of the Royalty.

The Inventor(s) responsible for Patent also receive 10% for lab expenditures.

.png?h=500&iar=0&w=500&hash=554BCAE6F646B48A88168B784B462F9D)

.png?h=500&iar=0&w=500&hash=34F59974F36E76CB4DD5909BCD2190FA)